Keywords: agri finance India, farm credit India, agribusiness finance 2025

What is Agricultural Finance?

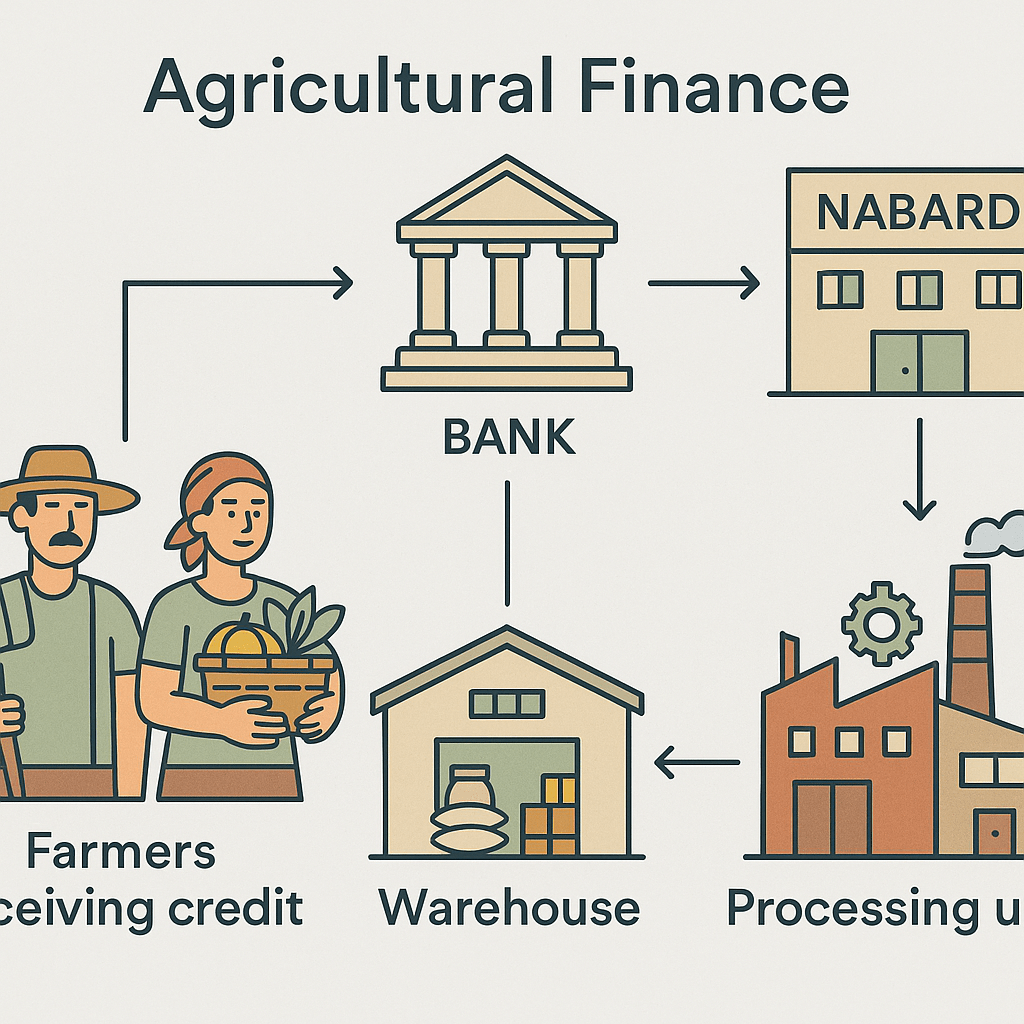

Agricultural finance refers to the financial services that support agriculture and agribusiness — including credit/loans, investment, insurance, subsidies, financial support for infrastructure, and risk management mechanisms.

Types of Agricultural Credit / Financing Needs

- Short-term Credit (0–1 year): for crop inputs (seeds, fertilisers, labour), working capital, input purchase.

- Medium-term Credit (1–5 years): for farm machinery, drip-/sprinkler-irrigation systems, plantation maintenance, minor infrastructure.

- Long-term Credit (above 5 years): for land development, orchards, dairy infrastructure, cold-storage units, agri-processing units.

Sources of Finance & Financial Support in India

- Commercial banks, Regional Rural Banks (RRBs), rural/cooperative banks — for farm loans.

- Institutional support via government schemes: e.g. infrastructure funds, credit-subsidy schemes, crop-insurance.

- Grants/subsidies for infrastructure under schemes like Agriculture Infrastructure Fund (AIF) — for warehouses, cold-storage, processing units, value-addition facilities.

- Finance for agribusiness start-ups, FPOs, and processing ventures — especially important for value-chain integration and agribusiness growth.

Importance of Agri Finance for Agribusiness

- Enables farmers to invest in quality inputs, technology, better seeds, irrigation — improving yields and output.

- Facilitates value-addition: setting up processing units, cold-storage, warehousing, packaging.

- Bridges the gap between small/marginal farmers and markets — via credit support, infrastructure building, and risk mitigation.

- Encourages entrepreneurship — agritech startups, food-processing ventures, logistics firms, supply-chain players.

Recent Policy & Sector Trends (2024-25) boosting Agri Finance & Infrastructure

- Government continuing support for schemes covering dairying, animal husbandry, crop insurance, and infrastructure — boosting rural incomes and agribusiness viability.

- Rising investment interest in input supply, agri-lending, agrochemicals, processed foods and agritech, seeing high profit-pool potential in coming years.

- Infrastructure funds like AIF supporting warehouses, processing units, value-addition centres — enabling better storage, reducing wastages, improving supply-chains.

Example Scenario (2025): Setting up a Dairy-Processing & Cold Storage Unit

Suppose a group of farmers or an FPO wants to set up a small dairy-processing plant + cold-storage in rural India. With proper financing (via bank loans + subsidies under AIF) they can:

- Procure high-quality milk from nearby farmers

- Process, pasteurize, package — value-add the milk

- Store and transport under cold-chain to urban markets / retail outletsThis creates jobs, increases farmers’ income, reduces wastage, and ensures quality supply to consumers.

Key Challenges & What Students Should Watch Out For

- Risk perception among lenders (weather risk, climate variability, small landholdings) — making credit access difficult for many small/marginal farmers.

- Infrastructure gaps — lack of warehouses, cold-storage, processing units, logistics.

- Fragmented landholding and small scale — difficult to aggregate produce/ demand for financing and scale economies.

- Need for strong support mechanisms, cooperatives or FPOs for aggregation and collective finance/ investments.

Conclusion

Finance and credit are critical pillars of agribusiness. They enable production, value-addition, infrastructure development, and entrepreneurship — connecting farms to markets. As agribusiness grows in India, understanding agri-finance mechanisms, sources, and challenges is essential for students and future agripreneurs

Leave a comment